This makes the residential sector nearly three times bigger than the $3.3 trillion superannuation industry and more than three times the size of the $2.8 trillion listed stockmarket. Housing also comprises roughly 62 per cent of authorised deposit-taking institutions’ balance sheets.

Confidence shock

The sharp drop in home values since the Reserve Bank started ratcheting rates higher last May has clearly shaken confidence, Owen says. “Household debt to income has ballooned to a record high of 146 per cent, which increased the risks associated with falling house values, especially as interest costs have increased,” she says.

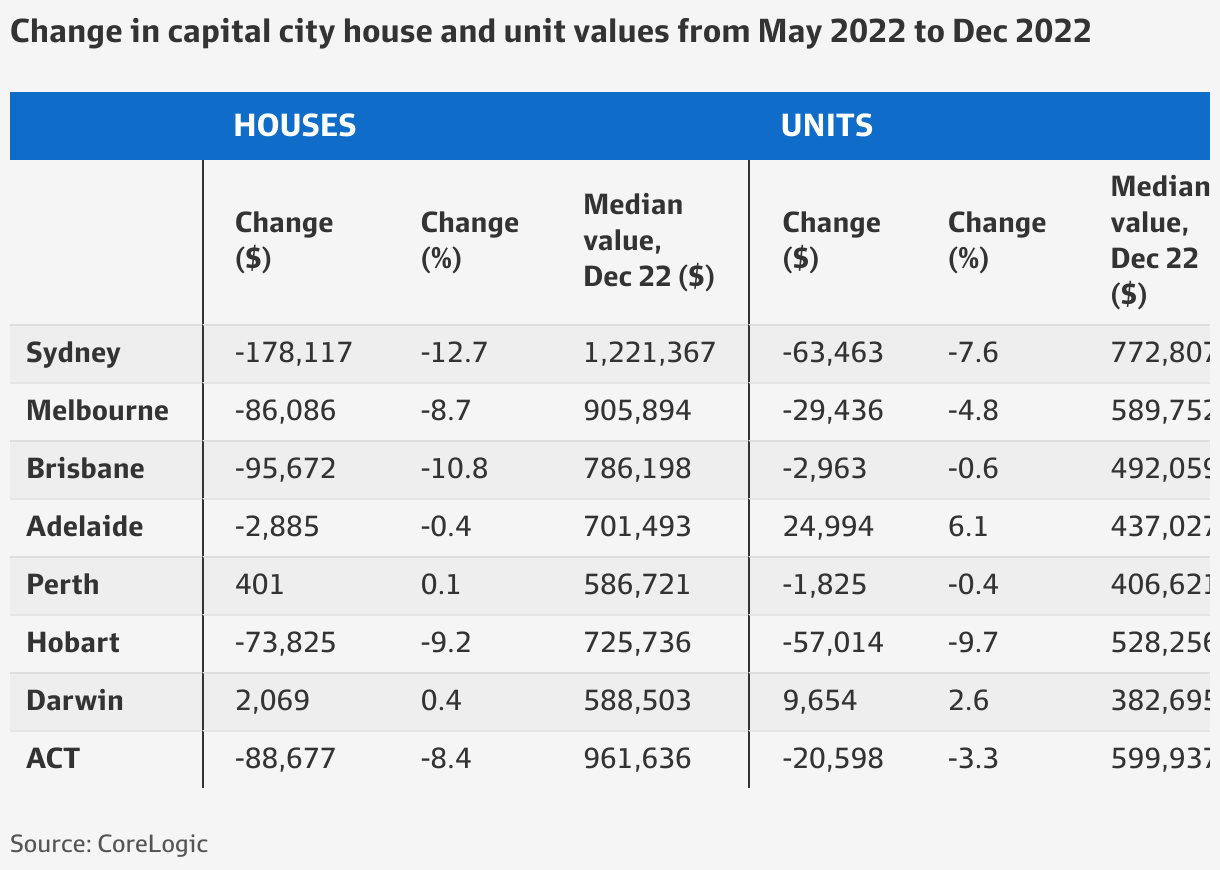

Since peaking last May, house prices nationwide plummeted a record-breaking 8.4 per cent early this month, fuelled by the most serious monetary policy tightening in more than 30 years.

Things could get a lot bleaker from here if the Reserve Bank of Australia further raises the interest rate to 4 per cent says Louis Christopher, SQM Research managing director. “If we go to 4 per cent, I believe we would see more forced selling activity in the second half of 2023 and that will drive prices down,” he says.

Many economists are expecting the Reserve Bank of Australia to raise interest rates another quarter-percentage point to 3.35 per cent in February and by the same amount in March or April, to 3.6 per cent. On May 1 last year, the benchmark rate was 0.25 per cent.

Shane Oliver, AMP Capital’s chief economist, says this could trigger another 9 per cent price fall by around September.

AMP Capital chief economist Shane Oliver.

“The main risks on the downside are that the RBA raises the cash rate to around 4 per cent as the money market is assuming, and the economy enters recession,” Oliver says.

“The RBA has already raised rates by more than the 2.5 per cent interest rate serviceability buffer that applied up to October 2021. In this scenario home prices could fall by around 30 per cent from their high.”

It’s a tough time to be a buyer. The eight consecutive interest rate rises have slashed borrowing capacity by about 27 per cent, while the soaring cost of living has made it harder to afford a mortgage repayment, let alone save a deposit to buy a home. Sellers are also having a difficult time, with fewer buyers looking to commit to big-ticket spending such as buying a home.

Recovery and rates

Undoubtedly, the housing market faces a rough year. But experts don’t rule out a potential recovery in prices if the RBA were to pause its tightening after February or March and starts cutting rates towards the end of the year.

“There’s a good chance that we’re getting close to the top of the interest rate cycle and the RBA could pause interest rate rises after February or they could hike one more time before pausing,” Oliver says. “They could potentially start cutting rates by the end of the year.”

SQM’s Christopher predicts that a pause in interest rates, such that they are on hold for the rest of the year, would be enough to fuel a lift in house prices by as much as 9 per cent in Sydney and 7 per cent nationwide.

This assumes interest rates peak at 4 per cent, inflation hits 8 per cent but falls back to 5 per cent, and the jobless rate rises but stays below 5 per cent.

”If the RBA were to hold [rates] below 4 per cent, given the surge in the economy that accelerated wage increases, I believe that will create grounds for a housing market recovery, albeit a soft one where we would see some single-digit house price rises occur in 2023, or at the very least, a situation where the housing market would stop falling.“

But the recovery could be delayed after house price falls reaccelerated in December. On average, it has taken 9 ½ months for national home values to move through a peak-to-trough decline, before values would start recovering.

“At least at the national level, no declines have lasted longer than 11 months, but this varies by region, for example, Perth home values were declining fairly consistently for over five years once the mining boom ended,” CoreLogic’s Owen says.

“This current downturn is just over eight months in, but doesn’t look like it has hit the bottom just yet. Housing value declines ‘reaccelerated’ in December, and this may continue through the start of 2023, as the cash rate looks set to rise a little further off the back of ongoing inflation.”

Eliza Owen at Corelogic says the housing market likely isn’t at the bottom.

During the housing market downturn triggered by the GFC in 2008-2009, prices took 11 months to bottom out and nine months to recover. The downswing of 2010-2013 took 20 months to bottom out, and 20 months to recover.

“It is possible that if prices bottom out with a peak in the cash rate midway through this year, then we could see a peak-to-trough period of around 15 months and take around as long to recover, but it’s not a hard rule,” Owen says.

An uncertain cycle

So, a lot is riding on the direction of interest rates and the health of the Australian economy.

“It’s very uncertain what the next growth cycle will look like, though we expect it will be a much more muted upswing than what we’ve seen through to 2010s and early 2020s,” Owen says.

“The last time Australia’s cash rate was over 3 per cent, national home values did experience a trough-to-peak upswing of around 16 per cent over 2009-10, but other factors such as strong overseas migration aided this, as did the dwelling market coming off a lower base, and being more affordable.”

This means the days when investors can count on house prices doubling every eight to 10 years could be over, says Owen.

“I think this is less likely in the 2020s than in the 2010s because the 2020s is the decade that’s bringing back inflation,” she says.

“If we get those ongoing spikes in inflation, we can pretty much wave goodbye to the pattern of interest rates moving reliably lower over a long period of time which has fuelled past price increases,” Owen says.

“This is not to say that real estate values won’t increase over the decade, as property prices tend to rise gradually over time in line with inflation, but high-growth areas may be harder to uncover, or require more research to find.”

The more likely scenario is for prices to return to their long-term average annual growth of 4.8 per cent over the past decade and 5.1 per cent each year over the past 30 years.

A question of supply

The federal government’s move to add supply of affordable housing could also dampen price increases in the years ahead, says independent economist Stephen Koukoulas.

However, he adds that there are other factors that could fuel a stronger recovery such as the growing population and undersupply of housing.

“This is somewhat of a tailwind for prices in the next few years, as the pipeline of new development approvals is trending 11.3 per cent below the decade average, which could lead to some undersupply in some dwelling markets,” says Owen.

“In nominal terms, housing may eventually get back to record highs as the market moves in line with inflation.”

Kent Lardner, founder of Suburbtrends, says a 10 per cent price gain could occur in select areas in 2023, but most markets are unlikely to enjoy any double-digit gains until late 2024.

“Prices have been erratic in the last 12 months, with an average peak to trough of 17 per cent based on the markets I’ve analysed,” he says. “When interest rates start to fall again, hopefully in 2024, we will see some solid gains as a result of the chronic undersupply of new housing stock and population growth.”

Desirable housing markets that suffered the largest decline and affordable areas offering quality lifestyle, could post the strongest rebound when prices start rising, says Lardner.

“If the gains between 2023 and 2024 match the losses of the last 12 months the average market could see prices improve by 17 per cent,” he says.

Lardner expects Sydney’s outer west and Blue Mountains to recover first, along with the inner west, northern beaches, Newcastle and Lake Macquarie, Adelaide-South, and the Gold Coast.

The Blue Mountains could be among the first markets to recover. Robin Powell

Owen also sees a quicker recovery in the more volatile, upper end of the market.

“Given that we’re going through a relatively sharp downswing, I think it’s reasonable that some of the more volatile markets could actually pick back up quite quickly,” she says.

“For example a 10 per cent uplift in some of the high end and central markets of Sydney and Melbourne over the space of a year or two seems reasonable, given they would be coming off the back of severe declines.

“However for some of the more affordable markets that have seen a large upswing and not much of a downswing through rate rises such as Perth and Adelaide, I don’t see those markets going through another 10 per cent increase on top of recent strong gains in a short period of time.”

Koukoulas says while the fundamentals supporting the housing market should boost a strong recovery, another housing boom is unlikely.

“I don’t think the dynamics for the resumption of the house price boom are in place at the moment,” he says. “You need a whole lot of things to go right for house prices to boom again.

“The fundamentals supporting house prices are there once we get to rate-cutting cycle, but we don’t know when that happens.”

Bagikan Berita Ini

0 Response to "Sydney property: Australia's $9.3 trillion housing question - The Australian Financial Review"

Post a Comment