When British real estate investor Graham Clemett bought McKay Securities in May, he had a clear plan.

He would split the UK property landlord’s assets in two, fold its office portfolio into Workspace, the property trust he manages, and sell off its warehouses.

But his idea has been thrown off-course.

“We’ve had lots of interest [from buyers] in the last six months or so. But people have come back and chipped the price to levels we don’t think are sensible,” said Clemett, who still owns roughly £150mn worth of warehouses. “It’s a bit of a distressed sellers’ market at the moment.”

Globally, commercial property landlords have been caught out in recent months as borrowing costs have shot up. Some lenders, unsure of where rates and property values will settle, are choosing to retrench.

The mood across the industry — which was relatively bullish at the start of this year — has darkened rapidly, with some high profile investors now warning of a lack of finance in parts of the sector.

“We are sitting in a market that is close to a credit crunch,” said Raimondo Amabile, global chief investment officer at PGIM Real Estate, an arm of US insurer Prudential Financial, whose fund is one of the biggest investors in the US, France, Germany and the UK.

“Banks are frozen . . . In Milan, London etc there is still finance, but costs are two to three times what they were a year ago.”

‘There is going to be a correction’

Having endured the worst period of the Covid pandemic, which emptied shops and offices across Europe and North America, commercial property investors were more optimistic as restrictions were rolled back this year.

But soaring energy prices and rapid inflation have meant real estate borrowing costs have surged since the start of the year, leaving a trail of collapsed property deals and spooked landlords.

The five-year Sonia swap rate, used by UK lenders to price loans, has risen fourfold in the past 12 months to 3.9 per cent.

Central bank rate hikes have also made commercial property less attractive on a relative basis: after a jump in September, 10-year UK government bonds were yielding more than property for the first time since 2007, according to MSCI, despite being less risky than offices or shops.

“There is going to be a correction,” said Mark Allan, boss of FTSE 100 property company Landsec, one of three UK listed landlords that reported valuation declines last week.

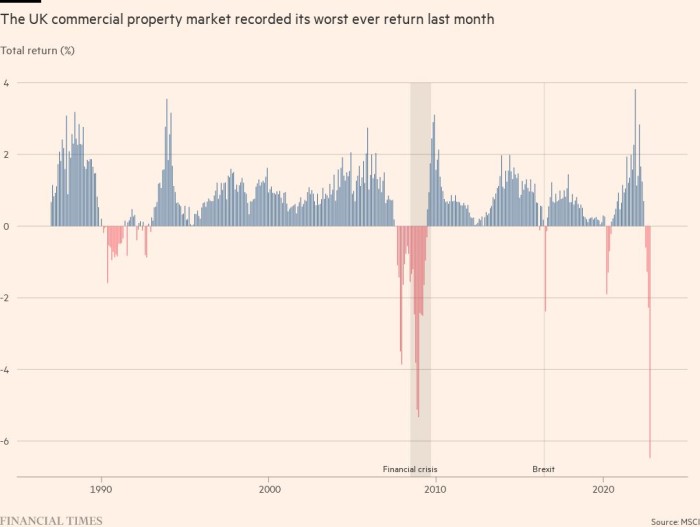

Last month the MSCI UK property index — which tracks shops, offices and warehouses worth tens of billions of pounds — fell by a record 6.5 per cent, eclipsing even the biggest monthly falls suffered during the 2008 financial crisis and Covid.

Allan said he would not be surprised if values fell 15-20 per cent in some areas, wiping tens of billions of pounds off the sector.

Offices among most exposed

Office landlords, still struggling with the fallout of the pandemic, are among the most exposed.

Occupancy rates are half pre-Covid levels in the UK, at just 30 per cent, according to Remit Consulting. England’s office stock is falling at the fastest rate for 20 years as employers reassess, according to an analysis of business rates data by law firm Boodle Hatfield.

Development costs have also rocketed. One big London office landlord said the cost of debt to fund a new development project had risen from 8 per cent to 14 per cent in the past two months.

“The whole capital markets have been hit, but real estate finance is far worse than anything else,” they said.

Parts of the US market are even more challenging. Amabile, at PGIM, said older offices with poor environmental standards were most exposed, particularly as more staff opted to work from home.

“The secondary office sector in the US is not uninvestable, but no one wants to finance it. There’s a belief that that’s a stranded asset,” he said.

Even newer offices could be endangered as job cuts in the tech sector reduced demand, he added.

When loans on older offices come due for refinancing “You will see such a drop in values that unless a borrower can put in a significant amount of equity they will have to pass the keys back, then the lender will bring that to the market at a distressed level,” said Jack Creedon, co-head of the real estate practice at law firm Ropes & Gray, whose clients include private equity houses and family offices.

“[We] could see 20-30 per cent of the existing office market wiped in the US. They will never get leased again.”

Lenders retreat

Fearful of writing loans against offices, shops and warehouses with tumbling valuations, many lenders are retreating and only signing off on the safest loans.

Real estate financing has traditionally been dominated by banks such as Barclays, Lloyds and NatWest in the UK, and investment banks including JPMorgan, Morgan Stanley and Wells Fargo in the US, according to Peter Cosmetatos, chief executive of the Commercial Real Estate Finance Council in Europe.

Insurers such as Aviva and Legal & General and private investors Blackstone and Starwood have become increasingly active in the post-financial crisis years. In the UK, insurers and other alternative funds now account for as much total lending as domestic banks.

Those still in the market today are narrowing their focus to trusted clients.

“Most lenders are still open for business, but it’s very much right asset, right sponsor, right price,” said Cosmetatos.

Jason Constable, head of real estate at Barclays Corporate Banking, said: “Barclays is a through-the-cycle lender in the real estate market and we will continue to support the right transactions for the right clients, on a risk adjusted basis to reflect the current macroeconomic conditions”

Alternative lenders are retrenching too.

“It’s just being responsible — we don’t want to lend to effectively lose money,” said one executive at a challenger bank.

It is a similar picture in the US, according to Creedon. With banks trying to pare back exposure to a sector on the turn, “a couple of clients are being asked by lenders if they are willing to buy loans against offices for 90 cents on the dollar,” he said.

Not as severe as 2008

Despite the pull back, commercial property professionals are seeking solace in a repeated refrain: this crisis will not be as severe as 2008.

“We’re completely wrong to think of what we’re seeing today through the lens of the [financial crisis],” said Cosmetatos. “Exuberant lending” from “homogenous sources” left both borrowers and banks exposed in 2008, he added.

Tighter regulation since has reduced the risks.

“I wouldn’t say there’s a credit crunch currently or one looming,” said Lisa Attenborough, head of debt advisory at Knight Frank Capital Advisory. “The debt market is in such a different place: you have got the banks, private lenders, insurers, overseas investors and debt funds — hundreds of them [able to lend].”

Whether borrowers can stomach higher interest payments is another question.

So far forced sales are not common. But some sellers do not have the luxury of sitting still.

“You are seeing funds facing redemptions and selling assets and those are available at attractive valuations,” said Simon Carter, boss of FTSE 100 landlord British Land.

Nick Sanderson, chief financial officer at London-focused developer GPE is one keen buyer, and is looking for about £900mn of deals.

UK property funds are selling off assets discreetly, he said: “it’s not a market where you put things out high, wide and handsome.”

Eventually, borrowers in the US and Europe will be pushed to the market because their mortgage terms are ending and they cannot afford to refinance at far higher rates.

Commercial real estate loans valued at roughly £150bn are due to be refinanced during the next five years in the UK, according to research by the Bayes Business School.

Bayes estimated there could be a funding gap of £27bn-£37bn when those loans come up for refinancing as a result of valuation falls.

In the US, Creedon anticipated there would be more distressed deals next year.

“We’re going back to the ‘old normal’. The last 10 years is the exception [with] money for free and ridiculously low rates. Are we in a new cycle? The answer is yes,” he said.

Additional reporting by Siddharth Venkataramakrishnan and Emma Dunkley in London

Bagikan Berita Ini

Related Posts :

Police seize beer cans potentially contaminated with meth in property raid - Stuff

Police seize beer cans potentially contaminated with meth in property raid - Stuff- China's property sector draws closer to exit from protracted slump - Reuters

- Property recovery seems to be underway - Chinadaily.com.cn - China Daily

- Investment properties on the chopping block as rates rise - The Australian Financial Review

- Gifts exceeding $300 to become state property - The Express Tribune

0 Response to "Commercial property values tumble as spooked lenders retreat - Financial Times"

Post a Comment